How to pay for school when you can’t

Paying for school sure can induce a sense-of-humor failure. But at Student Health 101 we had to find an upside, so here it is: The cost of higher education is an opportunity to build certain vital life skills—like stress management, financial self-empowerment, damage limitation, and problem solving. We’re confident these skills will be at least as valuable to you as your degree is. To get started, check out what students wish they’d known about loans, scholarships, and grants.

studentvoice

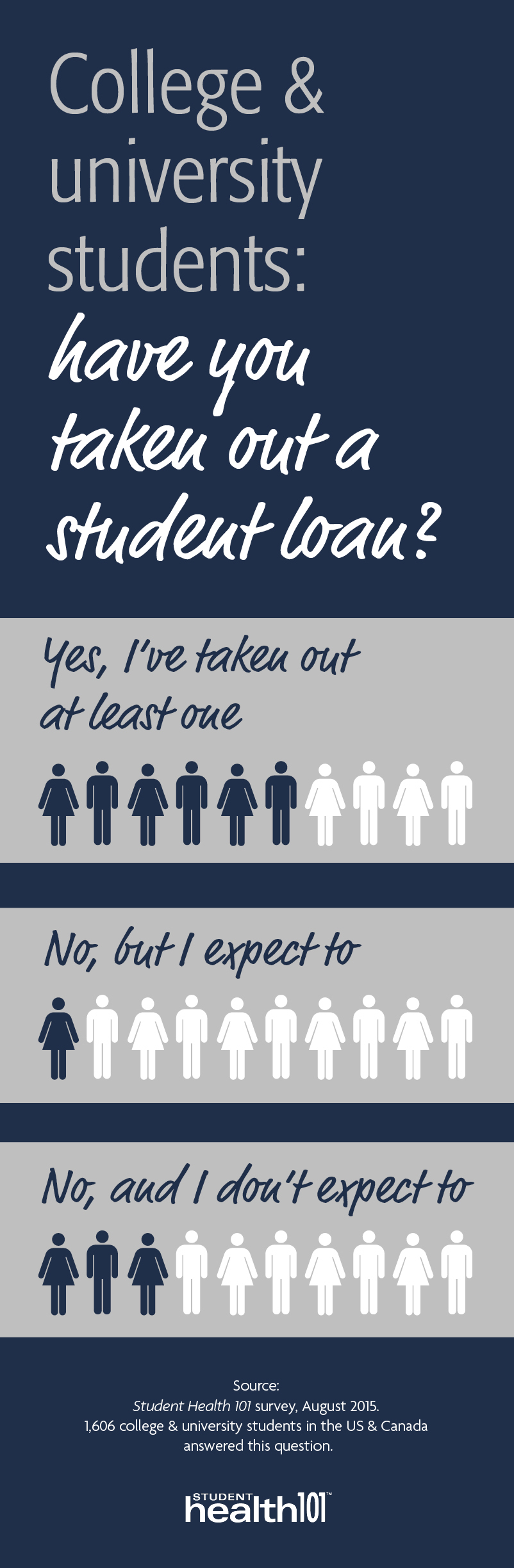

Student loans come in many shapes and sizes

“I wish I would have done my research and realized sooner that there are multiple options.”

—Graduate student, University of Wyoming

- The federal government offers several types of student loans.

- Private student loans are provided by banks, credit unions, state agencies, and other lenders.

- All loans must be repaid.

Gobbledegook overwhelm?

“I wish I’d known more about what different things mean: variable interest rates, deferment, deferral, etc.”

—Graduate student, Suffolk University, Massachusetts

Translate loan language into English

Translate loan language into English

Checklist

“Look at when the interest starts accruing, how much interest will accrue in school and later, and how long it will take to pay it off at what monthly payments.”

—Undergraduate, University of Alaska Anchorage

- Know when you’ll be expected to start making payments.

- Know what your minimum payments will be.

- Know whether your interest rate is fixed (never changes) or variable.

- Know when interest will start to accrue.

- Know your grace period (how long until you’ll start making payments).

- Know whether your loan gets you a tax deduction.

Subsidized vs. unsubsidized

“[I didn’t know] the difference between subsidized and unsubsidized government loans, as well as the payback rules.”

—Undergraduate, Utah State University

- The federal government provides subsidized and unsubsidized loans.

- Direct subsidized loans are available to undergraduates in financial need. The interest is paid by the government until you’re done with school.

- Direct unsubsidized loans are available to undergraduate and graduate students; there is no requirement to demonstrate financial need.

Get organized

“Always keep contact with your provider so you are more informed about your options, deadlines, and other important info.”

—Graduate student, University of Calgary, Alberta

- Keep track of loan amounts, providers, etc. This helps with your taxes, loan repayments, and self-empowerment.

- Read the info carefully. Don’t miss a deadline.

- If possible, start paying on the interest as a student to keep rates lower later.

- Routinely track your spending.

Reconsider how much you need

“Don’t take out loans if you don’t need to. I took out too much, and now I’ll have to repay them when I didn’t need them in the first place.”

—Graduate student, school withheld

- Check out the “cost of attendance” info on your school website.

- Take out as few student loans as possible.

Don’t miss your repayments

“It will hurt your credit if you are behind in payments.”

—Graduate student, Pittsburg State University, Kansas

If you don’t pay on your loan, you will go into default. This can negatively affect your credit score and reduce your options for getting a cell phone, or buying or renting a place to live.

Scholarships

“I wish I’d known how readily available scholarships are, if you just look for them.”

—Student, Normandale Community College, Minnesota

Student story

Felecia Hatcher was awarded $130,000 in scholarships. Her advice: Focus on what you’re great at or what you love, and apply for local scholarships: “The pool is so much smaller.” Hatcher is author of The “C” Students Guide to Scholarships (Peterson’s, 2011).

- Scholarships are usually merit-based. Some scholarships support students facing challenges or contributing to their communities, or employees of certain companies.

- Scholarships don’t need to be paid back.

- Check regularly for opportunities others miss with the office of financial aid or the scholarship office, and online.

- Apply for scholarships every year, even if it didn’t work out last time.

Grants & paid positions

“I wish I would have known about other alternatives before I signed away to be $30,000 in debt.”

—Graduate student, California State University, San Bernardino

- Grants provide free* money for college (*usually).

- The federal government offers grants based on need. You will need to complete the FAFSA (Free Application for Federal Student Aid).

- Check for grants with your office of financial aid or the scholarship office, and your academic department.

- Also look for grants from your state or local government, non-profit organizations, and research and travel programs.

- Apply for grants every year, even if it didn’t work out last time.

- Ask about work-study jobs, residential advisor (RA) positions, and other paid part-time roles.

Essential info from the US Dept. of Education:

Students’ stories

"I wish I’d seen the big picture"

“I knew in high school that a family member was going to cover all my expenses for college, so I didn’t pay attention when they were explained my senior year. But after two years there was family drama and they dropped my funding. I had about a month to learn everything I needed to know about loans and get two federal direct loans and a private loan. Should have paid attention.”

—Undergraduate, Pacific Lutheran University, Washington

“I just wish I had applied for more scholarships. It took me until grad school to start doing that.”

—Graduate student, University of Southern Maine

“’I didn’t realize how easy it was to just accept [loans] and how hard it was to pay them off. The available amount looks great but just makes you stuck with more debt!”

—Graduate student, California State University, San Marcos

“[I wish I’d known] community college is cheaper and I could work before I got to school. Also the average amount of years it would take a person in my financial situation to pay off a loan of the size that I took out.”

—Undergraduate, Western Illinois University

"I wish I’d known this earlier"

Without looking it up, could you say how long it will take you to pay off your loan?

- Yes: 63%

- Guesstimate: 26%

- No idea: 12%

Source: Student Health 101 survey, August 2015.

“I wish I’d known that I should pay off unsubsidized loans before subsidized loans.”

—Undergraduate, Western Washington University

“If you take a break from school, there is only so long you can defer your loans even if you are trying to get back in school.”

—Student, Rowan–Cabarrus Community College, North Carolina

“I wish I’d known that each student is allotted a certain amount of federal aid for the whole course of his/her undergrad education, which means students have the potential to run out of federal aid if they need an extra year or two.”

—Undergraduate, University of Massachusetts, Dartmouth

“I wish I’d known about income-based repayment plans. If so, I would not have had semesters with no textbooks or a shortage of toilet paper.”

—Graduate student, Western Illinois University

“I wish I [knew] the importance of paying off the principal as I attended school. This really helps in the long run!”

—Undergraduate, University of Wyoming

“I wish I knew how much I owe, how to pay it off as I go, how much they’re growing in interest, and how long it will take me to pay off!”

—Undergraduate, Roger Williams University, Rhode Island

"What I’d do differently"

How quickly could you locate the details of your student loans?

- Right now; it’s all in one place: 60%

- Give me an hour; it’s sort of organized: 29%

- Give me a day; I’d need to search: 9%

- Help! Could be anywhere: 3%

Source: Student Health 101 survey, August 2015. 200+ students answered this question.

“I wish I would’ve taken the time to establish a weekly plan so I don’t graduate so worried.”

—Student, Algonquin College, Ontario

“While I knew that you could pay them off while in school, I did not, and I wish I had taken advantage of the option.”

—Graduate student, school withheld

“Vote for a legislature and government officials who will work for lowering student loan interest rates.”

—Graduate student, University of the Pacific, California

“I honestly could have afforded to pay for more classes out of pocket instead of accumulating extra debt. I need financial aid, but a few of my courses I wish I paid for out of pocket because I could have.”

—Online student, State University of New York at Oswego

studentvoice

|